The Value of Surrender!

An Insurance for Afterlife!

LIC and SBI are by many leagues the two biggest financial institutions in the country and surprisingly have a similar size. Though SBI has a slightly bigger balance sheet of Rs 55tn to LIC’ Rs44tn, LIC may be the custodian of a greater amount of the savings of the aam aadmi.

Both offer a platform for parking one’ savings. Assuming an individual has a recurring annual surplus out of her earnings, the money can be deposited in the recurring deposit of SBI or paid as a policy premium to LIC. ( LIC and SBI used to connote a bank and a life insurance co.)

However, SBI would receive the deposit and represent it as a liability owing to the individual concerned but LIC would treat the same as an income and would not recognize a direct liability in the name of the policy holder!

This difference has a substantial salience should the individual wish to withdraw the contribution from either of them. SBI would return a sum not less than what was cumulatively deposited, may be marginally more; but such may not be the situation in the case of LIC! This is a general proposition subject to exceptions and not binding in all scenarios.

Why is it that the LIC is not in a position to return even the actual sums contributed periodically, though the said sum should have actually earned some minimum return for the institution over the time it was in its possession?

This brings in to focus two aspects. One is an economic factor and other an operational matter.

The economic factor is that the contribution made to the LIC periodically is to secure an insurance cover for the individual in the event of the death of the person anytime when the contract is kept alive.

The facility of the insurance cover carries a cost as the insurer assumes a risk to pay a sum far higher than the amounts cumulatively received should a death claim arise.

Hence, the contribution has two parts; one is towards the cost of the provision of the life cover which is a sunk cost to the individual and the balance is an investment like a bank deposit.

Ideally, it should be possible to indicate upfront to the individual the ratio in which the premium will be apportioned such that the insured knows the amount of the sunk cost and the portion remaining as her savings with the institution.

Unfortunately, this does not happen in most situations, though certain types of policies like linked policies may provide some clarity.

The reason that this doesn’t happen is due to the way the life business operates.

A bank deposit is invariably a direct transaction between the depositor and the bank. No intermediary exists to be compensated.

The insurance transaction goes only through an intermediary. The intermediary gets a commission on the entire amount which substantially comprises the savings or the capital.

This structure of the insurance industry where the agent gets paid for mere collection of the savings of the individuals that too at very high rates is the cause of the major wedge in the way the LIC assesses the returnable portion vs SBI.

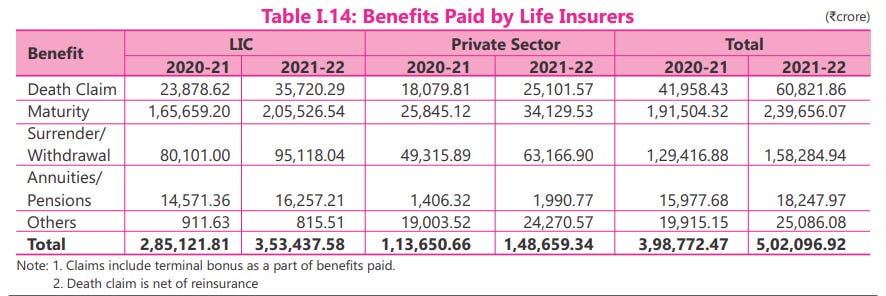

How rare is the occurrence of a termination or surrender of a life policy before its maturity? The statistics obtained from the IRDAI’ annual report depicted below seem to suggest it is quite common.

The third row that gives the data on surrender and withdrawal is the relevant one to notice. The readers can work out the proportion and assess.

In fact, the ratio for the private players has some messages which can be duly inferred without the article having to go at length on that aspect!

This aspect of surrender and the consequential loss to the savers has hardly been agitated as a matter of major concern hitherto. Associations that claim to represent savers have done little in this regard.

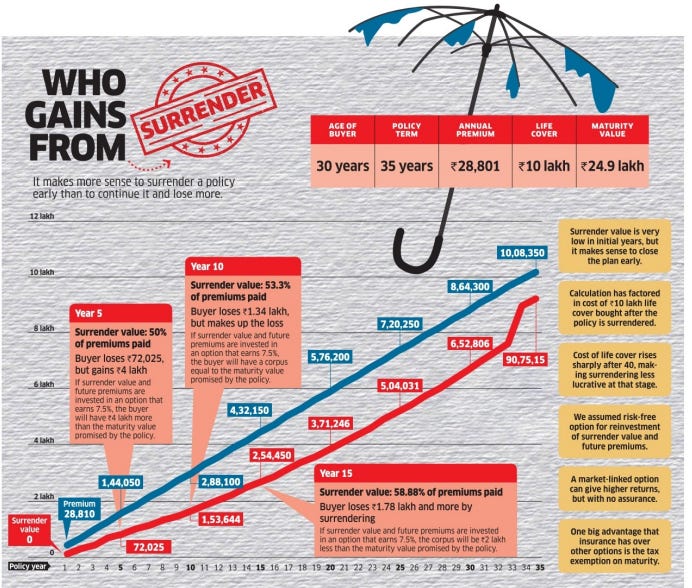

The real impact and the loss to the savers is brought out graphically in the picture below which appeared in the ET-wealth on 25th Dec2023-

Even the IRDAI has taken almost a quarter century since its inception to get alive to this matter. Last week it has come out with some proposal to change the equation a little more in favour of the savers.

It is only to be expected that the industry is not happy with this and will apply pressure to dilute this. Given that the behemoth LIC is a listed entity and its market valuation would suffer where the GoI holds almost 95% equity, would make this not an easy change to effect!

Even these proposals are only ad hoc and do not go to the root of the issue. The main issue is that the cost of providing an insurance cover year on year should be clearly known to the individual covered and the contributions should be duly apportioned.

The insurer should recognize the premium portion as its revenue and the remaining deposit should be accrued in the discrete account of the insured. The annual income earned and apportioned to the concerned category of policy should be credited to the capital balance. When the surrender request comes the amount payable is transparently known.

In the event of death the amount payable would be the sum assured which is partly held as the deposit of the individual and the balance to be topped up from the provision for such contingency created annually based on actuarial principles.

This may partially be the case in some participating and linked policies but should become the pattern across all categories of policies.

Once this approach finds favor, the agent’ remuneration should be worked out only on the premium portion and not on the capital sum.

The selling of insurance has become so remunerative that the banks are fully focused on selling insurance and often at the cost of the core banking service.

A bank customer in most cases is highly vulnerable to be mis-sold investment ideas as there is an implicit trust in the bank manager who is met almost on a day-to-day basis. Many customers shun visiting the bank less due to the advent of digital banking but more to escape being thrust with the latest insurance product!

The surrender value issue is not peculiar to India but a structural issue in the industry across the globe. However, in countries like the US, it is possible to sell the life policy to life settlement companies that generally pay much higher than the surrender value.

These companies invest in unmatured policies like a mutual fund investing in debt or equity, and pay the premium on behalf of the insured and get the sum assured when the insured dies. These life settlement arrangements are yet another asset class to invest for HNIs as the return is quite steady and better than fixed income.

In the Indian context the only alternative to surrender is to assign the policy to the PF trust of which the insured is a member so that the future premium outgo is avoided as the PF fund would pay the same. This may be limited in applicability as it helps only PF subscribers.

For an average income earner, the three popular destinations to put away the savings are banks, life insurance companies and mutual funds. Strangely, each is governed by a different regulator and follow a different approach to procuring and managing the money.

While the suggestion is not that a single regulator should oversee all the three, and thereby incur the wrath of a multitude of bureaucrats manning these, it may be good if some common practices evolve across the three for the protection of the innocent investors.

The doctrine of surrender is part of all the religions. Christmas is not an inopportune time to contemplate on this though the object of this surrender is just seeking more money!

Some out of the box thinking from your side.