Rane!! Steering Swerves Suddenly!!

Does the scheme rationale gaslight the minority?

Till the year 2004-5, Rane, like most Indian family-owned groups had evolved as a conglomerate with new ventures being created out of the surplus funds available in existing businesses leading to cross holdings, leaving some degree of vulnerability for the promoter if there emerged a determined raider.

In 2004-5 the group commissioned a restructuring exercise taking some inspiration from a more nefarious idea that Bajaj group adopted to make the operating entities come under a financial holding company with more than 50% control so that the operating entities were free of any potential takeover threat.

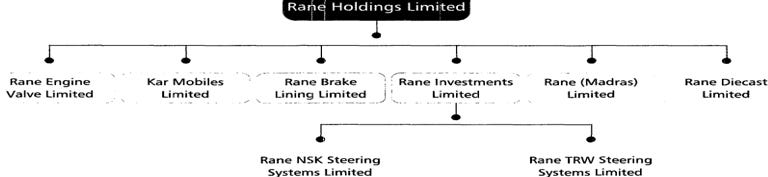

Keeping out the minutiae of the steps undertaken, which may at best interest an acdemic, the structure that emerged resulted in the three publicly listed operating entities, Rane Madras Ltd (Rane-M) Rane Brake Linings Ltd (RBL) and Rane Engine Valves Ltd (REVL) becoming subsidiaries of Rane Holdings Ltd (RHL).

All the three entities prior to the new structure had public shareholders with more than 50% interest. In the new construct the public holding dropped to less than 50% and the promoter’ interest through RHL, moved beyond 50%.

However, in RHL the promoters held less than 50% and the public more than 50%, which remains almost unaltered till date.

While the contention would be that the economic interest of the promoter and public was left unaffected pre and post restructuring ,as the public was compensated with shares in RHL for what they sacrificed in the three operating entities, the loss of the majority status in the operating entities that typically command a premium in the market cannot be overlooked.

A holding company in the Indian bourses goes at a discount. It is often a facilitative vehicle for the promoters to acquire the public cheaply and finally delist as one of the investment vehicles in the TVS group did.

However, the justification for creating the structure was not acknowledged as done to protect the promoters’ interest, and instead the usual spiel of how the structure freed the individual businesses to grow exponentially with the overall support of the group’ financial prowess was sold.

Fast forward the calendar by sixteen years, the group on 9th Feb2024 discovered a fresh merit in turning the steering wheel 360º by announcing the integration of all the three businesses, this time by bringing it under a single entity, proposing the merger of REVL and RBL into Rane-M.

This time the filings to the exchanges wax eloquent on the synergies that can be better tapped in a single entity as catalogued in the explanations (a) to (i) giving the reasons for the merger.

However, one of the reasons is actually logical provided the group is willing to go the whole distance like vehicles fitted with its parts do, and not sputter and stop half-way as planned now!

“Consolidation of shareholdings in a single listed entity will align interests of all the shareholder groups and allow them to participate in the growth prospects of a larger diversified auto component player.

This reason has real merit since the public shareholders have an interest in regaining the status that they enjoyed before the restructuring done between 2004 and 2008.

To accomplish this wholesomely which would make all shareholders equal in status, both the promoters and the public, the holding company RHL should also be collapsed in the process to consolidate all the shareholders in a single structure.

The public holding that is truncated between the new single operating entity Rane -M and RHL is value destructive and even the tenuous raison d'être for RHL in the past is no more tenable with Rane-M being the sole entity listed. The JVs that are unlisted can exist under Rane-M.

It is also to be noted that RHL pulls money out of the group entities through trade mark fee and service charges for common group corporate services. This is also a reason for impacting the profitability of the operating companies. The holding company deriving a royalty or trade mark fee was a trend set by the Tata group with limited legitimacy. Even that trace of legitimacy is absent in Rane’ case.

The financial snapshot of the group below may help to wind up this part of the discussion.

There is no doubt that the group is not in good shape operationally, and urgent measures are needed to improve the situation.

However, it is not apparent to an outsider that when the three companies are under the watch of an identical team of Chairman and Vice Chairman, with the boards having many common directors and having a common corporate set up run by RHL, what undiscovered synergy will surface by a simple legal act of merger!

Do the directors believe that the merger is a real solution for the operational weaknesses, or is there a promoter angle to it, like a few cases of family related arrangements that happened in the TVS, Murugappa Group etc., in the recent years?

This angle is purely speculative and lacks any basis in the information available in the public domain. The promoter holding is split between two groups in the third and fourth generation of the founder’ family owning 22.49% and 24.09% respectively in RHL.

If some understanding has come about to let one of the families to own the entire stake, then perhaps the individual entities may be unnecessary and a single entity may do.

Another possible reason for the proposal could be the fact that Rane -M has recognized a significant deferred tax asset due to the losses arising on its overseas investments caused by the dismal performance of the North American business.

The merger of the three companies may be a strategy to accelerate the use of the tax loss, assuming that a loss on a capital reduction can be set off against the normal business profits.

The next part of the discussion is on the process.

The following is the composition of the boards of the three entities involved in the merger.

The meetings to approve the merger took place as under.

It is difficult to conceive that the above meetings were the only occasion the merger discussions took place. Even a super over in a T20 match takes more time! Intriguingly RBL filed its exchange intimation even before the meeting of the transferee company concluded!!

It is unlikely, and would amount to levelling a serious charge of misconduct to assume that the meetings done on 9th February were the only discussions had by the directors on this topic!

The SEBI’ Circular dated July13,2023 on disclosure of material events / information by listed entities under Regulations 30 and 30A of Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015, suffers from a major lacuna that it mandates disclosure only when a final decision is taken by the board of directors on key corporate developments like restructuring etc.,

Major corporate actions like mergers take a few weeks if not months of preparations including engaging outside consultants and experts like valuers. Unless the board gives an in-principle clearance sharing of data like future projections is not possible.

The board ought to have held discussions spread over many meetings on the alternatives available to improve the business performance and a single meeting for fifteen minutes cannot conclude such nuanced discussions even after considering the caliber of the directors involved!

In fact, fifteen minutes is the minimum for the bearer, however quick footed, to serve the tea and cashew nuts!

In effect, many people inside and outside the company have been privy to the deliberations. Only the outside investors and the stock exchanges got to know it on 9th Feb.

Is the merger a done deal as the promoters have over 70% holdings in two of the three entities and in REVL it is about 59%?

A corporate lawyer opined that clause b(ii) of para 10 of the SEBI master circular dated 20 June 2023 may attract for this scheme, requiring a e-voting by the public shareholders before the scheme can be filed in the NCLT and a majority approval of the non-promoter shareholders is a pre requisite.

Recently, the non-institutional public shareholders of Butterfly Gandhimathi Appliances in a rare case of acting in unison derailed the scheme of merger with Crompton, its holding company. Ironically, the institutions had voted in favor!

Among the three entities the public shareholders of REVL currently having 41.68% voting share would get significantly diluted in the merged entity.

A group of public shareholders with 41.68% voting strength affords a greater chance to stall a special resolution that requires a 75% vote, as compared to a lower public holding that would arise in the merged entity. This veto right possibility is a valuable right that will get upset in the new structure.

In a lighter vein, the smart way to obtain an unanimous approval shall be to merge RHL as well in the current scheme!!

To conclude a verbose narrative, when a corporate chieftain thinks that both additions(mergers) and subtractions(demergers) represent a completeness in the strategy, there is no contradiction, as she is only echoing what the rishis of yore said -

They took only spinning the toss time in a cricket match rather than consuming super over time.