Quess, Quizzed on its Tax Quest!!

Questions loom on the governance quotient!!

The NFRA punishing a chartered accountant for lapses in professional work has ceased to make news like the cricket scores!

Such being the case, why would a listed company that clocked a turnover of Rs17185cr in the FY2023, inform the stock exchanges of such an insignificant issue as a CA getting penalized for Rs50lacs, when some of its peers fail to inform about FIR filed against the Chairman, unless pressed by the exchanges?

Quess Corp Ltd has been hit with tax demands disallowing its claim for tax exemption under section 80JJAA of the Income tax Act consequent to the surveys held at its offices in 2021.

In the course of such proceedings the tax authorities found the certificates supporting the claims issued by CA Pawan Jain incorrect and reported the matter to NFRA.

The NFRA proceedings lists the alleged wrong or the excess claims by the company,

The NFRA claims no jurisdiction to decide the validity of a tax return. Its order is valid only to the extent of the lapses identified in the work of the CA.

The company has every right to defend its case dehors the findings of the NFRA. However, it is but natural that the observations in the order would subtly affect the perception of the appellate authorities about the bona fides of the claim.

Before moving ahead, it is essential to set the context and highlight the materiality of the tax demands.

The company has acknowledged a contingent liability of about Rs175cr in its communication to the exchanges, but the NFRA order allenges a total sum in excess of Rs1000cr as wrongly certified!

Quess’ net profit in FY23 of Rs222cr is just a tad above 1% of its consolidated topline. The tax under dispute appears to be many multiples of a full year’ profits; in fact, exceeding four- or five-years’ profits!

Though the NFRA order affects just an individual professional, the findings of the lapses that led to the imposition of the fine flag questions on the larger aspect of the governance architecture in the company to deal with compliances. The indictment of the CA is also indirectly a rap on the knuckle of the company and its statutory auditor.

It is also relevant to note that besides income tax, multiple other legislations impact the business operations of Quess like the different labor laws, indirect taxes etc.,

The above underscores the level and intensity of the oversight demanded of the audit committee, the statutory auditors and the board of directors with regard to statutory compliance, the maintenance of accounts, data and documents.

Unlike a family-owned company that has an over-weight of family members in the board often leading to a personalized style of decision making subverting the collaborative and consultative style of a board’ functioning, Quess’ board has a clutch of independent professionals.

Given that the income tax claim under dispute has an outsized bearing on the reported results and can viscerally impact the market valuation, the logical expectation is that the board and the statutory auditor would have spent substantial time to study the law, understand the facts, look at the supporting documents, get sufficient external validation before making a decision to claim the benefit.

The NFRA order refers to many contentious aspects to the claim indicating that it was not such a simple matter of interpretation. The indicated level of complexity should have necessitated obtaining a legal opinion on the issue from a lawyer or a retired judge.

An external legal expert typically acts as a devil’ advocate, to challenge the company’ stance like a tax officer or a court would, to test the soundness of the proposition and independently validate the documentary support.

Even after doing a thorough exercise, the board must have anticipated a possible rejection by the tax authorities and looked at the consequential profit and the cash flow implications.

Similarly, the statutory auditor should have looked at whether a part provision should have been protectively made to absorb any shock.

The role of the statutory auditor in this exercise is of utmost salience. Any position taken on taxes has a direct impact on reported profits and is closely correlated to the share prices.

Any multidisciplinary audit firm would have an independent tax team to validate the documentation and the legal interpretation before the audit team would pass the tax provision number.

The auditor has a much higher professional and moral responsibility on such decisions even as compared to a CA actually putting his pen to paper to certify the tax filings.

It is only legitimate that all of the above would have been duly documented to be available for reference should personnel change and problems surface at a much later date.

In the instant case the doubt that arises is how much of the diligence and discipline was observed by all concerned?

The reason to raise this is due to the observations in the NFRA order that certain basic facts were not checked and validated. Without laboring this with details, if the company and the statutory auditor had followed the process fully, such documentation should have been readily available for the certifying CA to complete his task.

There was either lack of access to the documentation for the CA, which is unlikely, or that the paperwork by the company and the statutory auditor was wanting.

A legitimate question to be asked of the audit committee is why was the certificate for a high value tax claim which is pinned on many factors arising entirely from the records and books of accounts entrusted to a different CA and not to the regular auditor?

Is it that the audit firm did not wish to stick its neck out to avoid the kind of embarrassment that the certifying CA suffered in this case?

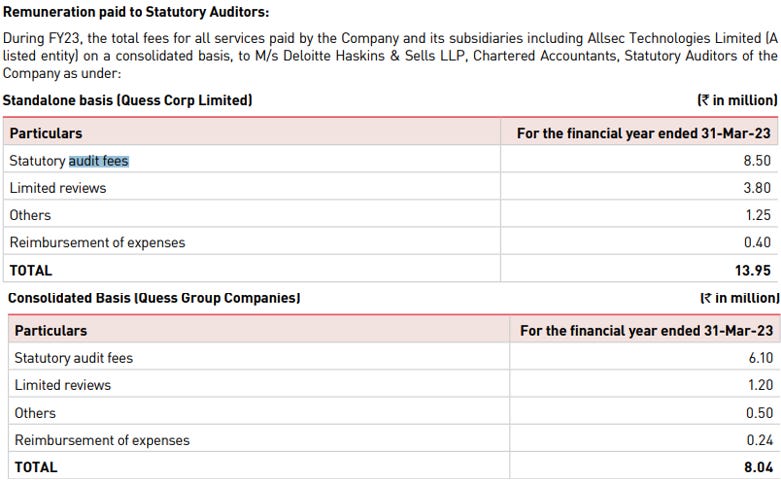

The fees paid to the auditors is given below.

If the auditor who was remunerated as above should have been reluctant to provide a certificate which is primarily fact and accounting based, it should have been a red flag for the audit committee and the board on the risks involved in the tax claim.

While deciding the issue, the NFRA should have called for the audit working papers to check if the documentation allegedly not verified by CA Pawan Jain was verified by statutory auditors for considering the claim in the tax provision.

The NFRA has just plucked the low hanging fruit in this case!